The Battery Bet That Changed the World

How China’s policy, BYD’s foresight, and an American invention reshaped global energy

Charlie Munger once described BYD’s founder, Wang Chuanfu, as a cross between Thomas Edison and Jack Welch. It’s an apt description. More than a century ago, Edison dreamed of creating a battery that could enable mass-market electric vehicles. He even worked with Henry Ford on a prototype.

But Edison was too late and didn’t succeed. The result was our addiction to oil and the complete dominance of the internal combustion engine, with all its profound implications.

Fast forward to the 21st century. Five years ago, that dream finally came true—not in Detroit, but in China. Two Chinese companies—BYD and CATL—commercialized a breakthrough in lithium iron phosphate (LFP) battery technology. Originally invented in the U.S., LFP batteries found their home in China, enabling safe, affordable, mass-market electric vehicles and disrupting the global auto industry.

But it didn’t stop there. The rapid scaling of LFP batteries also drove down costs, making them viable for energy storage—solving a key problem that had bedeviled renewable energy since the days of Edison: how to store intermittent renewable energy for use when you need it.

Looking back, 2020 was a pivotal year. How did it happen?

But first, the top stories I’ve been reading this week:

The Essential Five

The China Association of Automobile Manufacturers has come out with a strong warning against a vicious price war in China’s EV sector after BYD cut prices. Link here in Chinese: “Since May 23, a certain car company has taken the lead in launching a substantial price reduction campaign, and many companies have followed suit, triggering a new round of ‘price war’ panic. Disorderly ‘price wars’ intensify vicious competition, which will further squeeze the profit space of enterprises, and then affect product quality and after-sales service guarantee, which will not only hinder the healthy development of the industry itself, but also endanger the rights and interests of consumers and bring safety hazards.”

According to data released by Cui Dongshu, Secretary General of the China Passenger Car Association, in the second quarter of 2025, BYD, Geely and Tesla held the top three global share of pure electric vehicles with a share of 21%, 12% and 11% respectively. Geely also launched its first self-owned roll-on/roll-off (RoRo) ship to export its vehicles, which is powered by LNG.

Caixin published an interesting commentary on the importance of China’s rare earth dominance: Commentary: Why China’s Rare Earth Dominance Matters More Than Ever.

UBS has warned clients that the brutal sell-off in lithium stocks is far from over, predicting that an oversupply of the battery material will continue to weigh on prices for the rest of this decade. Story in the AFR.

Interesting Linkedin post and article by Abhishek Kumar on why US battery startups fail. He predicts “that the U.S. is likely to become irrelevant in the battery race, echoing past experiences in steel, solar, and other sectors. The West bets on “next-gen” innovation to bypass Asian manufacturing, but without a strong industrial base, scale is impossible.”

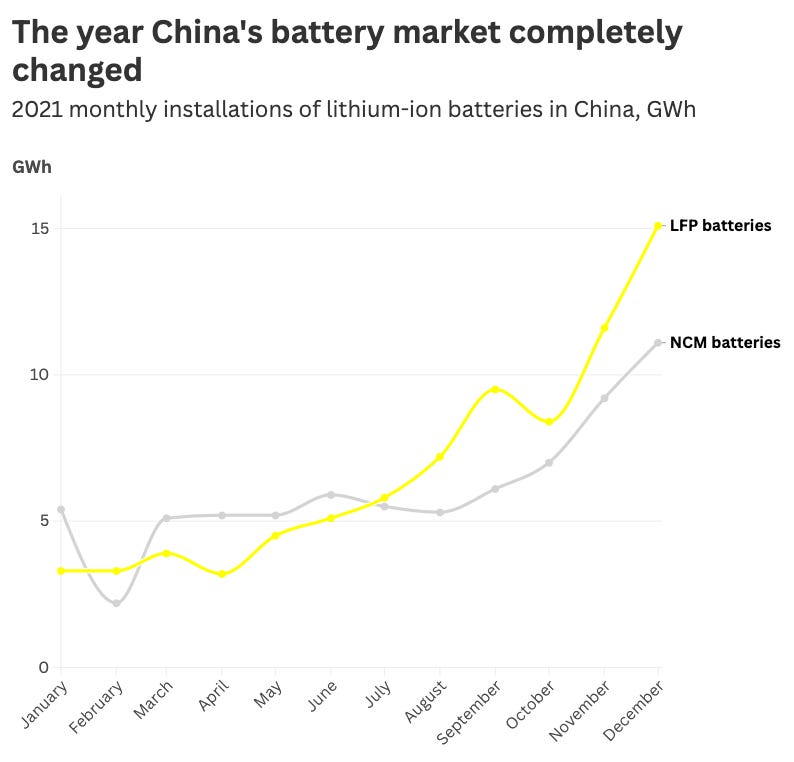

A Chemistry Shift—and a Market Shock

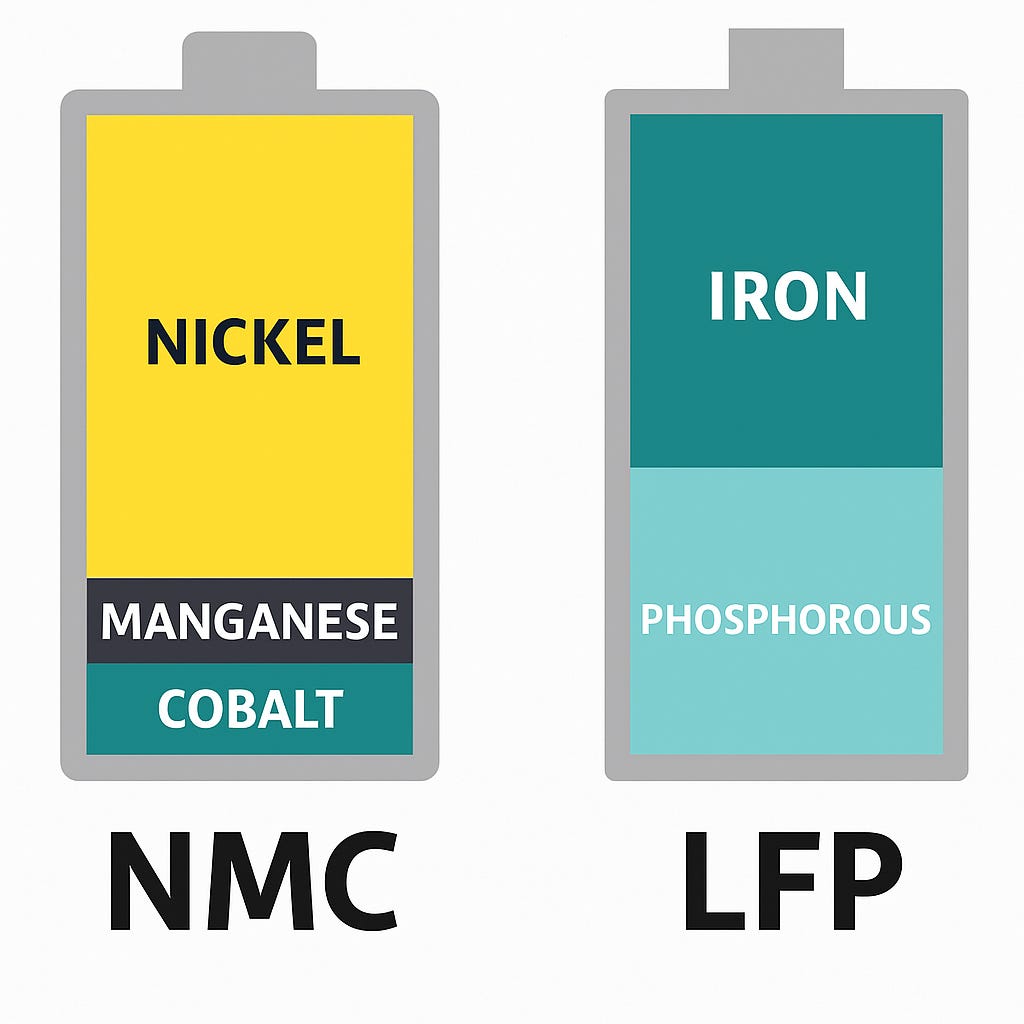

In just five years, China’s EV market flipped the script on battery technology. Back in 2018, 80% of China’s EVs ran on nickel-cobalt-manganese (NCM) lithium-ion batteries. These batteries are mostly made up of nickel, a metal mostly mined in Indonesia, with cobalt from the Democratic Republic of Congo.

Today, less than 20% do. Instead, LFP batteries—without nickel and cobalt—dominate. BYD and CATL lead the charge.

This shift caught most analysts by surprise and it rattled global supply chains. It meant less demand for the minerals of resource-rich countries like Indonesia and the Democratic Republic of Congo.

NCM lithium-ion batteries have higher energy density meaning they can power cars further on one charge. In 2020 people thought that range anxiety was the key problem holding back EVs. Analysts predicted that LFP batteries would make up between 15% to 40% of the EV market by 2030. That now looks like a big underestimate.

Innovation, driven by policy, shifted the entire market.

Western Automakers Scramble to Catch Up

Today, foreign automakers are racing to adopt LFP technology. Volkswagen plans to use LFP batteries in all its ID series cars to cut costs, aiming to bring prices below €25,000. “In the volume game, LFP is the technology,” said Volkswagen CEO Thomas Schäfer.

Even South Korea’s battery giants—LG Energy Solution and Samsung SDI—announced plans this week to build LFP production lines in their U.S. plants with General Motors.

It all began in 2020, as the world was reeling with the impact of the Covid-19 virus. A battery revolution was about to erupt in China.

Designed in the US, Made in China

LFP battery chemistry was first discovered by the Nobel-Prize winning American scientist John Goodenough, who filed a patent for the chemistry in 1997. Later research at the University of Montreal and Hydro-Quebec coated the LFP cathode with carbon, increasing its conductivity, and this patent was filed in 2000.

In hindsight, what happened in the West is not directly relevant to this story, since LFP was never properly commercialized or produced there.

In China, however, BYD’s founder Wang Chuanfu saw the strategic potential, according to a recently published book on BYD, The Soul of Engineers, 工程师之魂. In 2002, Wang asked his team to explore LFP batteries as a way to avoid dependence on nickel and cobalt imports—a lesson learned from China’s oil dependence. In a pivotal meeting, Wang declared: “That’s the one!”

In 2008, BYD launched the world’s first LFP-powered car, the F3DM, followed by the K9 bus and the e6. However, by 2017, Chinese government subsidies had begun to favor higher energy density nickel-based batteries, pushing LFP to the sidelines. Battery makers rushed to produce nickel containing batteries to get the subsidies. BYD was out of luck.

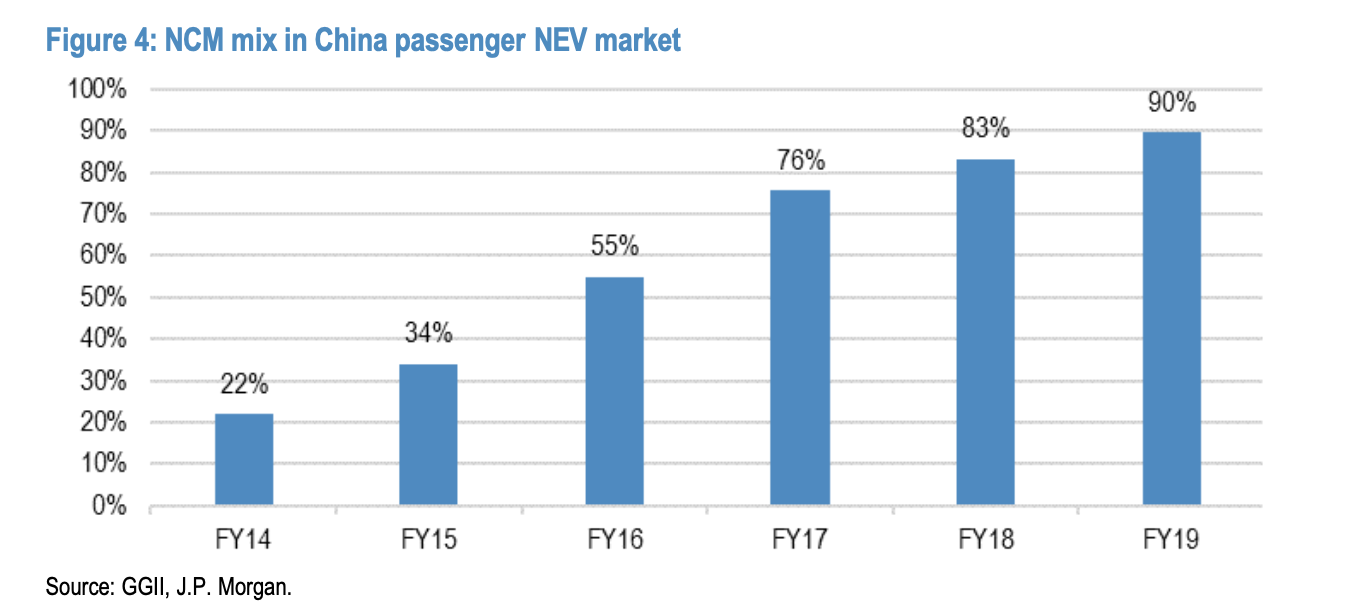

In 2017, for the first time the share of NCM batteries in China’s passenger EV market exceeded less powerful LFP batteries, with the share of LFP falling to 26%. Foreign battery makers were much more advanced in producing higher energy density NCM cells.

NCM batteries were completely dominant by 2019, as you can see in this chart:

But Wang believed that safety was the priority - not chasing higher energy density, according to the Soul of Engineers book.

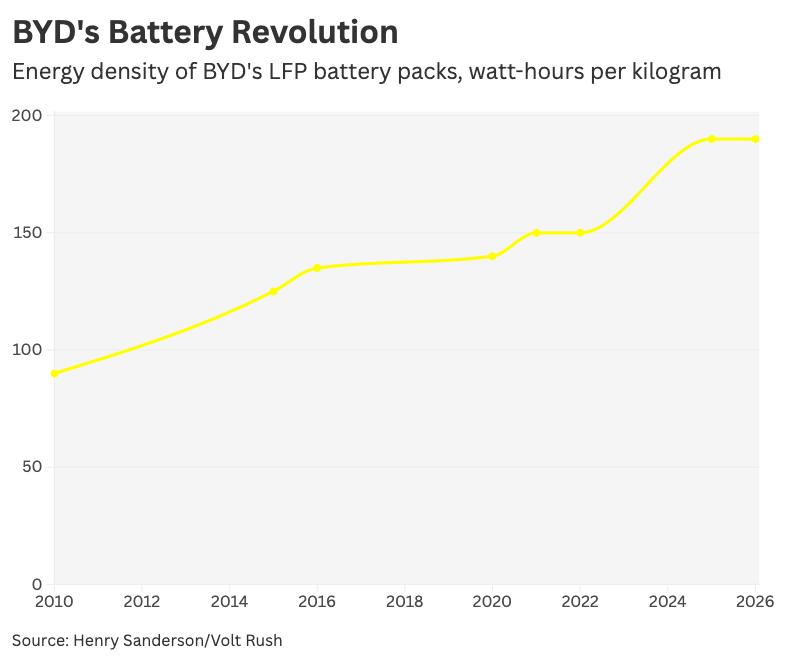

So BYD innovated. It developed the Blade battery—thin, modular, and structurally integrated. This cell-to-pack (CTP) design removed excess materials, boosting energy density while maintaining LFP’s core advantages: lower cost, better thermal safety, and longer life. I wrote about them for the FT back in the day.

And then Chinese policy changed - setting the stage for BYD’s victory.

Shifting to Cost

In early 2020, China changed its EV subsidy structure, to focus on cost over performance. The government set a new maximum pre-subsidy vehicle price.

Tesla announced on April 30, 2020 that it would cut the pre-subsidy price of its standard-range Model 3 made in China from CNY355,800 to CNY291,800 to maintain eligibility for the national subsidies. Elon Musk also announced it would use CATL’s LFP batteries in its China-made Model 3.

The same year BYD released the Han EV, powered by its Blade battery.

By the end of 2020, BYD and CATL controlled 66% of China’s LFP EV battery market, up from just 6% the year before—a stunning reversal. Western battery producers were left completely cut out.

It would take a further five years for the West to catch up.

The Power of Policy—and Patience

The story of LFP is a case study in how industrial policy, vision, and engineering pragmatism can shift global markets.

Here are three underappreciated lessons:

Policy isn’t just about subsidies—it’s about direction. China didn’t just pour money into EVs. It shifted criteria and rules in ways that forced change.

Incremental innovation wins. BYD didn’t invent a new battery. It re-engineered and optimized an old one. That mattered more than moonshots.

Forecasts are fragile. Most analysts missed this shift. The next one may already be brewing in unexpected places.

After 2020, BYD’s growth accelerated. By 2021, BYD had produced over 1 million vehicles. It had taken 13 years. It then took just a year to get to 2 million cars. Then half a year to get to 3 million, and then just five months to get to 4 million.

A battery revolution that started with Thomas Edison’s dream finally found its moment in China. Wang Chuanfu’s big bet on LFP batteries didn’t just power a new generation of cars—it ignited a race that’s reshaping geopolitics, supply chains, and the very future of energy.

Excellent overview about tech direction change from NMC to LFP, I would see another game change happening from LFP to blend LMFP with NMC and Hybrid Na-ion batt tech in the coming years.

This is a fantastic deep dive into the LFP battery story and BYD’s strategic role. Given how policy shifts and incremental innovation reshaped the entire global battery landscape, where do you see the next big breakthrough or market disruption happening in EV battery technology over the next five years?