Why we keep using the wrong chart on critical minerals

China’s real leverage may come less from refining dominance than from its overwhelming share of global industrial demand.

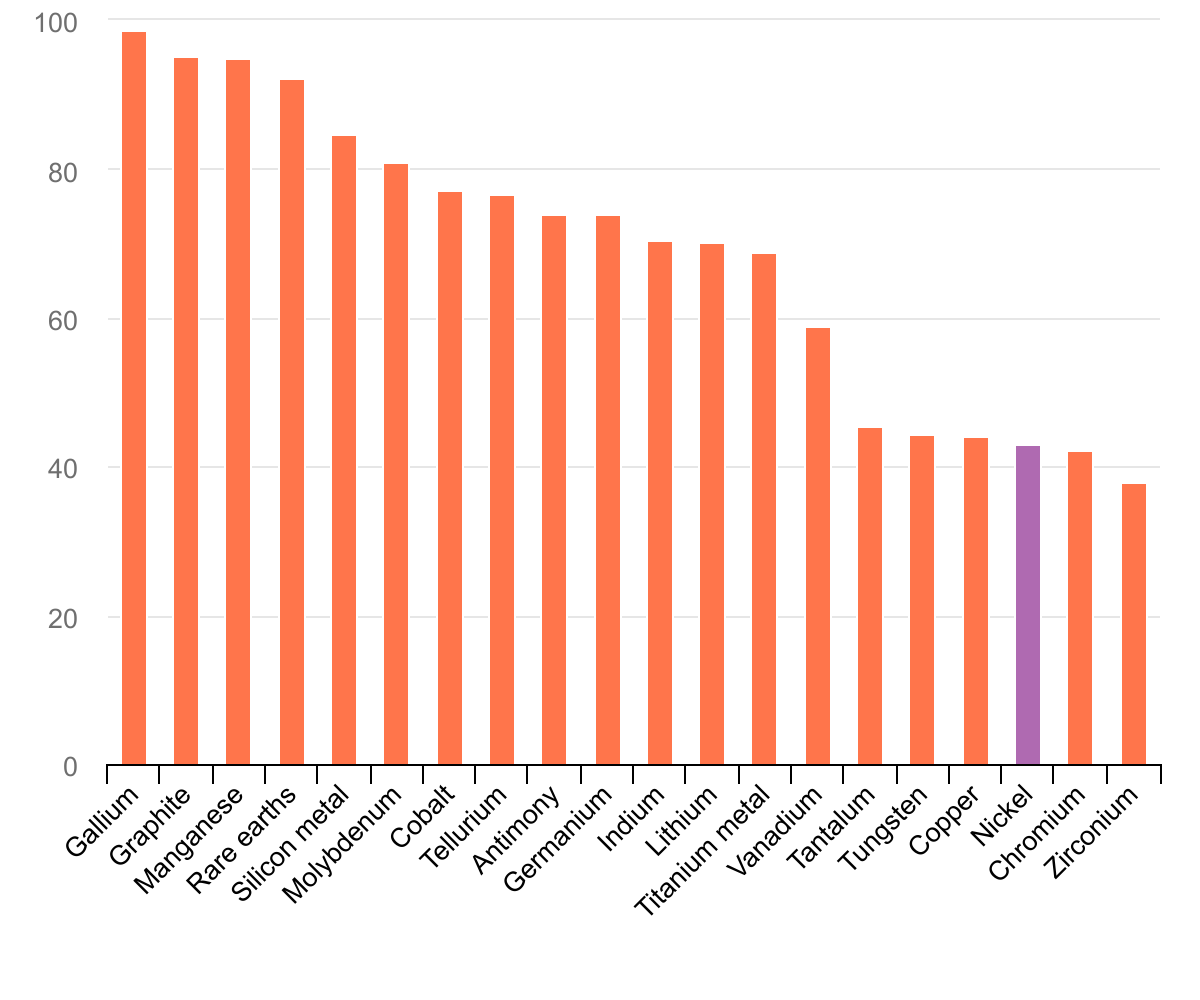

The most popular chart in the critical minerals world shows China’s dominance of refining and processing. It appears in almost every presentation on energy security and usually points to the same conclusion: China controls the supply chain.

I’ve used the chart myself. But increasingly I think it points us toward the wrong conclusion.

Two numbers illustrate why. According to the excellent lithium analyst Daniel Jimenez, China consumed 87% of the lithium mined globally last year. The US and Europe together consumed less than 3%.

In rare earth magnets, Chinese exports to the US in 2024 (before China’s export controls last year) were around 7,400 tonnes, around 3% of China’s total production.

Why are we so obsessed with China’s share of production rather than its share of consumption?

The historically important story is not simply that China amassed such a large share of critical mineral production, but that it amassed such a large share of global industrial demand.

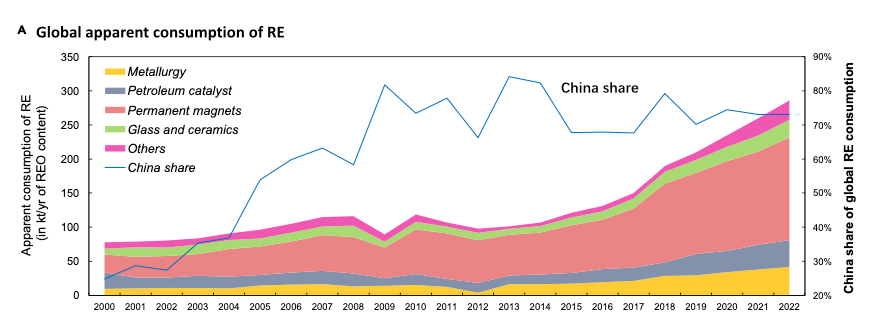

You can see this clearly in rare earths. China’s share in global consumption increased from 25% in 2000 to over 70% in the period 2018–2022, according to one recent study.

During the same period US consumption of rare earths declined from around 11,000 tonnes a year in 2010 to only 2 kt/year in 2011, and then remained stable at between 9–10 kt/year during 2020–2022, which is equivalent to only 4% of China’s consumption level, according to the study published in One Earth.

China didn’t become a Saudi Arabia of critical minerals exporting processed minerals to the rest of the world. Far from it. It became a net importer of rare earths while the US became a net exporter.

The problem was not simply that the United States lost rare earth mining to China after 2000. It was that it lost the demand for rare earths.

Buying finished products

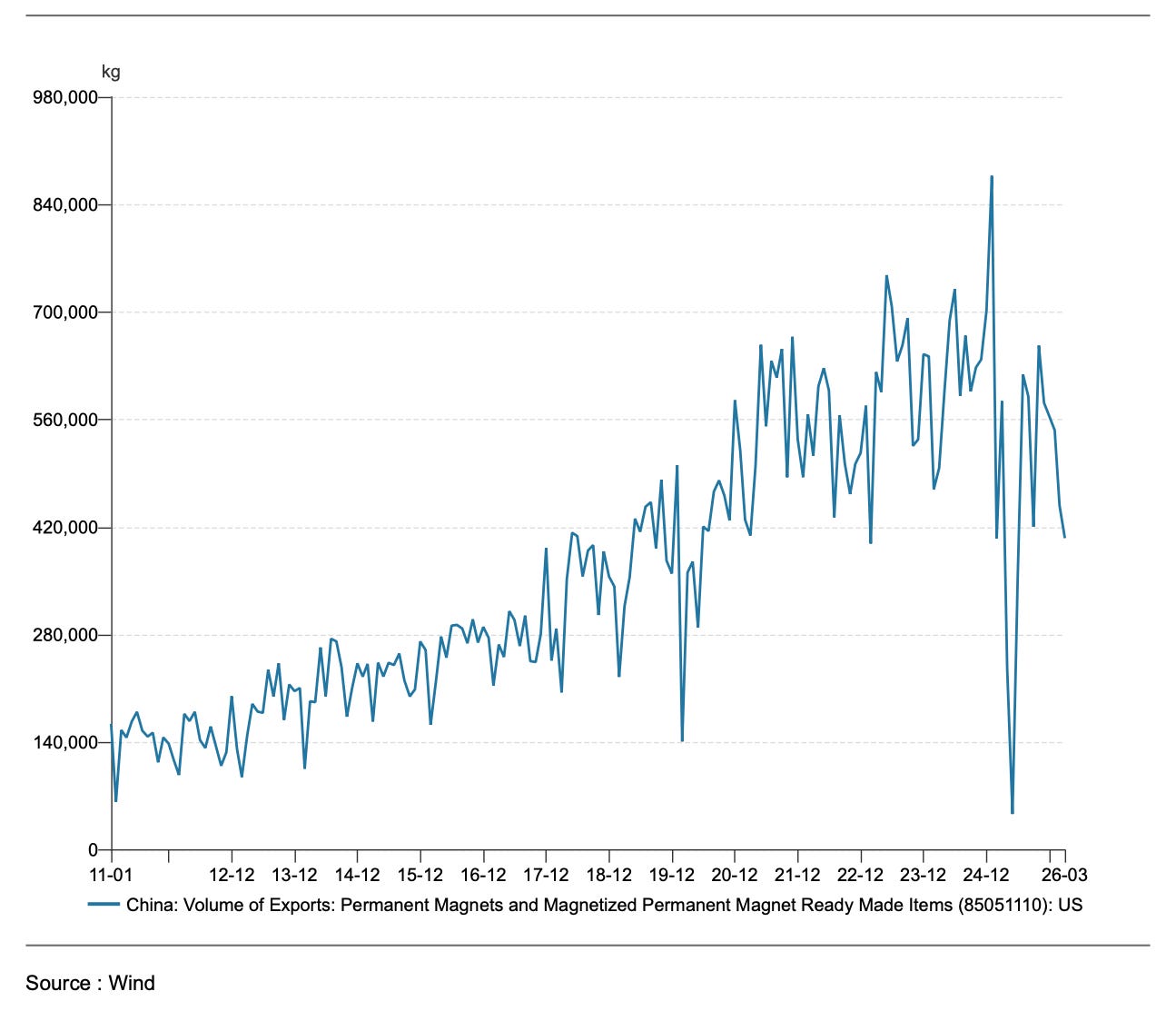

In return for its exports of rare earths to China the US began importing Chinese rare earth permanent magnets, imports of which roughly quadrupled between 2011 and 2024.

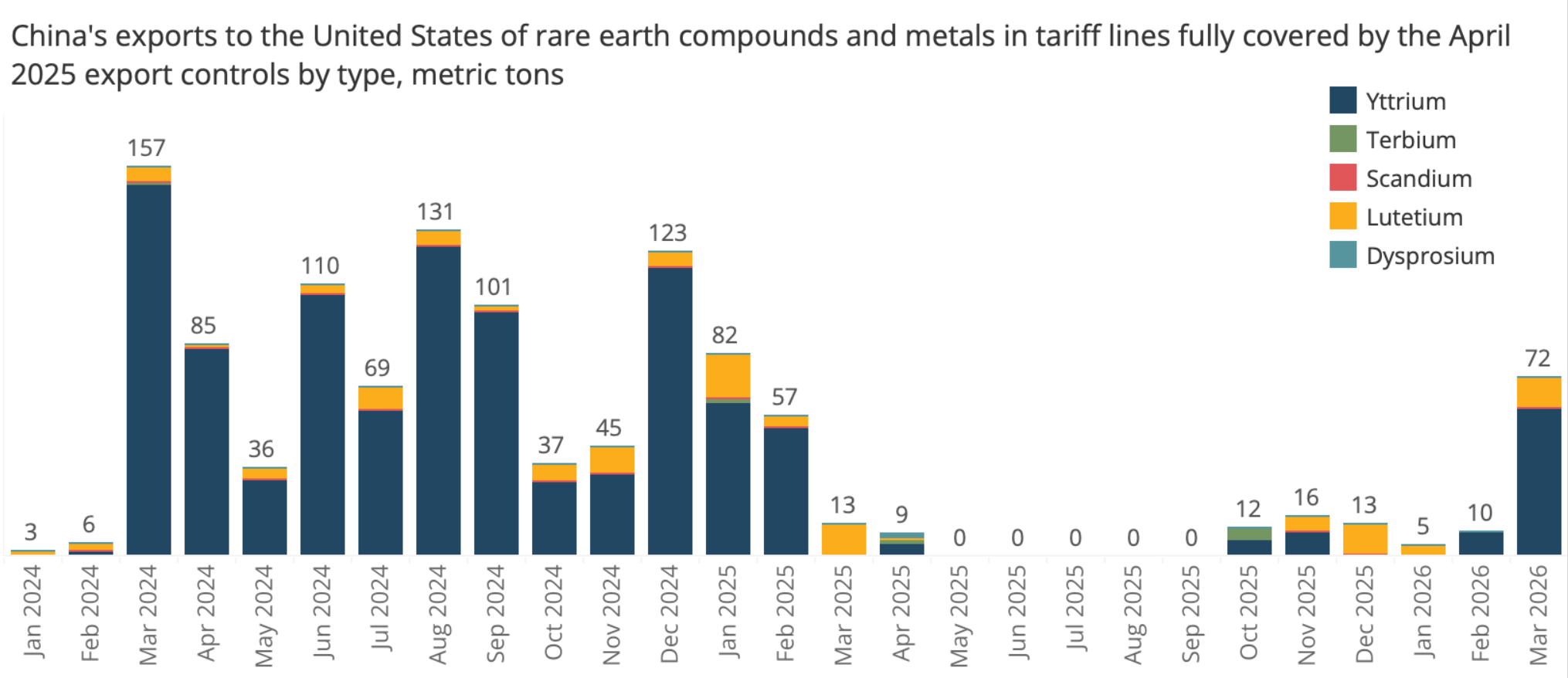

China’s export controls last year hit exports of these magnets, as you can see in the above chart only acclerating efforts by the US to build its own production capacity.

But the controls were precisely targeted. China's total rare earth magnet exports fell only marginally in 2025 — from 58,142 tonnes in 2024 to 57,397 tonnes — a drop of less than 2%, according to SMM. Beijing didn't restrict global magnet supply. It restricted supply to one customer that represents around 3% of its production, while the rest of the world kept buying.

Overall China’s rare earth magnet exports are expected to increase this year, according to SMM, to 67,500 tonnes.

The US could produce enough magnets for its own demand without impacting China’s overall share of global production by very much.

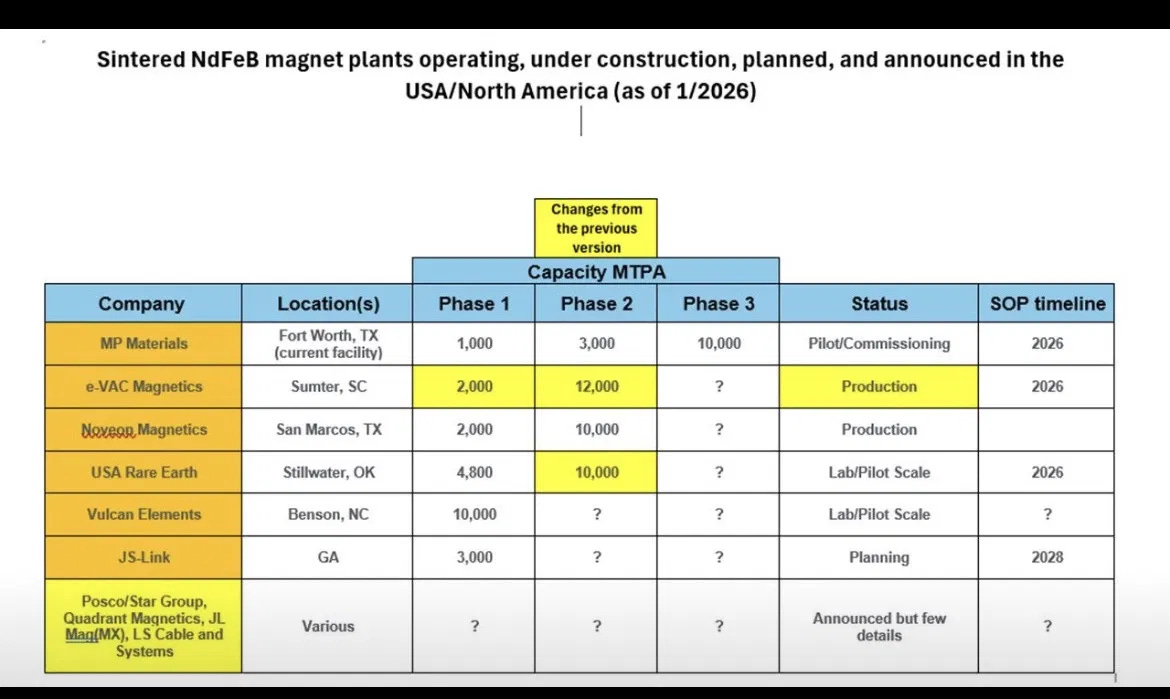

Magnet expert John Ormerod has a brilliant chart of all the planned capacity coming online in the US.

Phase 1 alone across the known companies totals roughly 22,800 tonnes a year. China’s magnet exports to the US were running at around 7,400 tonnes annually in 2024. So the announced Phase 1 capacity is three times current import levels. If it were all built and running, the US could be self-sufficient in magnet manufacturing.

Yet SMM forecasts China’s magnet production capacity was over 265,000 tonnes in 2025 and it is only increasing because China is meeting an increasing share of global demand (outside of the US due to tariffs) from exports of goods higher up the value chain, such as electric vehicles.

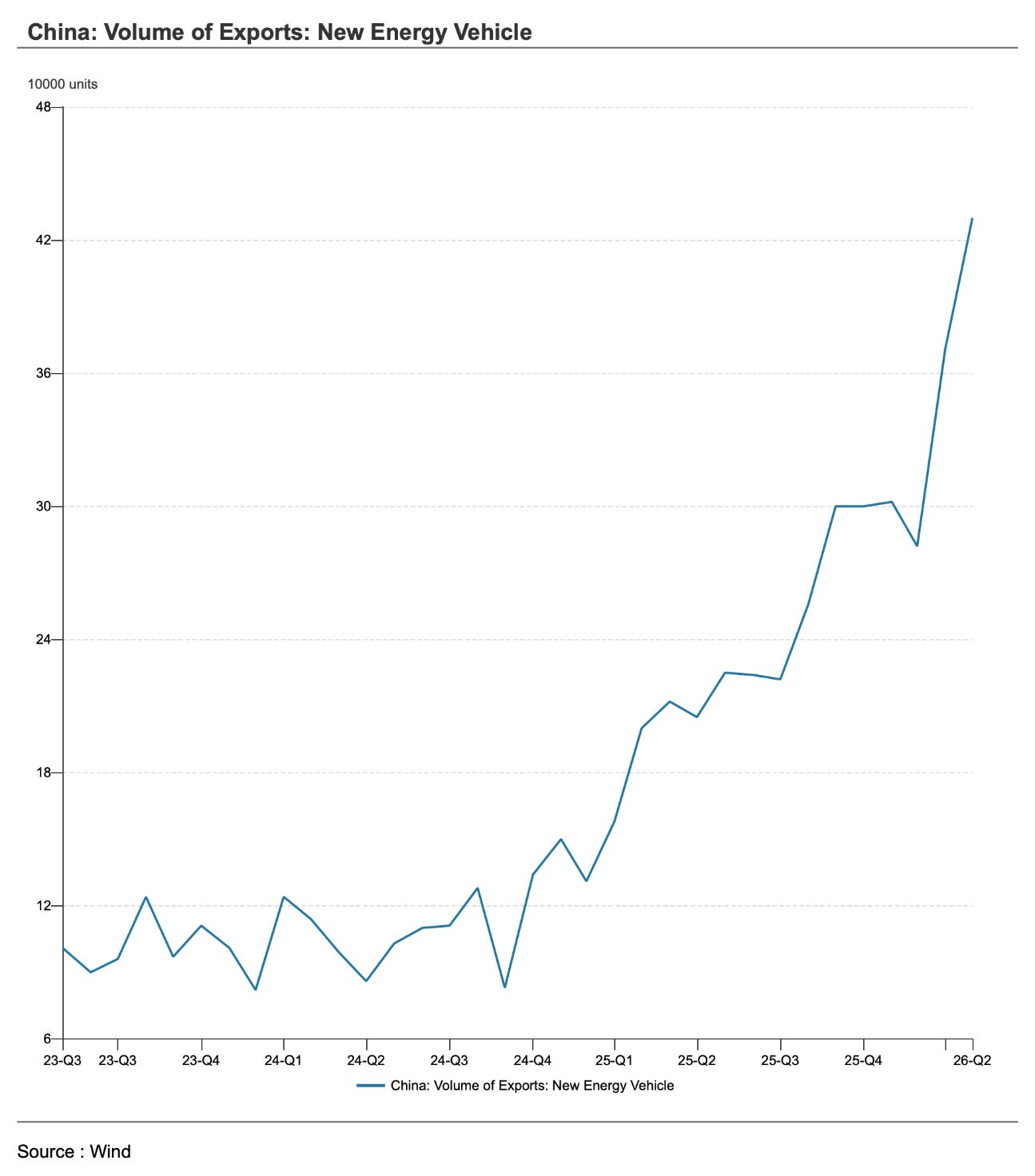

China’s rising exports

China’s exports of new energy vehicles (EVs and plug-in hybrids) doubled in 2025 to over 2.6 million vehicles, and in April 2026 jumped by 110% in one month alone.

Each electric vehicle contains between 2 and 5kg of rare earth permanent magnets, meaning China's surging EV exports are effectively a vector for rare earth consumption that bypasses the element and magnet trade data entirely.

It is no coincidence that the day President Donald Trump left China, Xinhua published an article about a new essay in the Party magazine Qiushi by President Xi Jinping saying yet again that “that the manufacturing sector is the foundation of the real economy.”

This export surge will continue. And as a result China needs to keep importing minerals to meet the global demand for electric vehicles and other clean energy technologies globally, which is only increasing following the Iran war.

The real question is how much ex-China demand for rare earths will be met not by elements or magnets, but by Chinese exports of finished products.

Export controls

Of course, the reframe in this post doesn’t dissolve every concern. For some materials such as heavy rare earths, germanium, tungsten, graphite the high level of Chinese supply concentration is the problem regardless of demand share.

If China is close to 100% of supply then as long as your demand is more than zero it is problematic.

But still, if the demand is small outside of China the solution in terms of ex-China supply is likely to be easier and less costly.

The US did not import large amounts of heavy rare earths from China, even before the latest export controls, according to this tracker from the Silverado Policy Acclerator.

Supply-side thinking

The deeper problem with the supply-share chart is what it does to Western thinking. It encourages policymakers to believe they have a supply problem when they really have a demand problem because the industries that actually consume minerals are in China. We buy the finished products.

The route to mineral security is not simply building processing plants in markets that consume less than 3% of global lithium chemicals. It is rebuilding the downstream manufacturing base — batteries, motors, and finished products — that creates the demand giving you commercial leverage with miners and exporters in the first place.

That is a far grander and more difficult industrial project in a world facing a wave of Chinese exports. But you cannot onshore your way out of a critical minerals problem when it is really about dependence on highly competitive Chinese manufacturing.

The demand-side reframe is the one that almost never gets made — and it changes the investment conclusion more than most processing-thesis bulls want to admit.

Strip out the government floor, the 45X credit, the FEOC restriction, and ask what the addressable market actually is for a US processor serving a domestic manufacturing base that consumes 3% of global lithium chemicals.

The harder question your piece raises isn't just about supply chains. It's about political architecture. China built its processing dominance through a 30-year state-directed commitment that didn't have to survive a midterm. The West is trying to replicate it with policy tools that expire, get repealed, and get traded away in the next budget negotiation.

If the demand base never onshores and the support gets cut before commercial viability is reached, the processing buildout isn't a solution. It's a very expensive bridge to nowhere.

Great post. Thanks for sharing this perspective